Dubai-based founder building the next generation of tax software for global businesses. I started in the world of accounting and finance, built a successful tax and advisory firm (Alpha Pro Partners), and then turned those real-world pain points into a product: Tax Star, an AI-powered platform designed to make tax filing simpler, faster, and more accurate.

Audit-Ready Financial Reporting in 2025: Tools, Standards & Best Practices under the UAE’s Evolving Tax Regime

August 2, 2026

Content

The UAE corporate tax regime is now in full swing. Auditors and reviewers want more than financial statements, they want a clear trail from trial balance to tax return, plus evidence that your numbers are complete, consistent, and locked after filing. From 2025, audited financial statements are expected in more cases, and Free Zone entities under special regimes have their own audit obligations. As more businesses adopt Corporate tax filing services, the expectations for clean documentation are rising. We wrote this guide to help you keep the process simple, fast, and calm, especially for Corporation Tax Small Business and Corporate Tax Free zone entities navigating new requirements.

The core standards, at a glance

Financial statements in the UAE are typically prepared under IFRS. Your corporate tax return bridges back to those same numbers with clear adjustments and support. For many groups and Corporate Tax Free Zone entities, audited financial statements are required from tax periods that start in 2025. If you are a tax group, special-purpose audited financials may be needed. If you are a Qualifying Free Zone Person, audited financials apply, with extra procedures in some cases. Keep your accounting base consistent, especially if you rely on Corporate tax filing services, and keep your return tie-outs clean for both medium enterprises and Corporation Tax Small Business structures.

What changed for 2025, in plain language

- Audited financials now apply more broadly. From tax periods that start on or after 1 January 2025, audited financial statements are required if your standalone revenue exceeds a set threshold, or if you are a Qualifying Free Zone Person.

- Tax groups prepare audited special-purpose financials. If you form a tax group, expect audited special-purpose statements in the format the Authority specifies, something often supported by Corporate tax filing services

- Some Free Zone activities have extra procedures. For example, distributors operating in or from a Designated Zone may have additional steps.

- Old thresholds or carve-outs that applied before 2025 may no longer apply. Review your 2025 obligations afresh and update your financial reporting plan to stay compliant, particularly if you are a Corporation Tax Small Business.

(If you want us to confirm your exact status and thresholds, we can check your facts and map your reporting path in a quick call.)

The audit-ready mindset

Audit-ready does not mean heavy. It means your numbers can be rebuilt in minutes and your evidence sits where anyone can find it. The keys are:

- One source of truth for the period close.

- A tight folder structure by year and period.

- Simple rules for cut-off, judgments, and related-party pricing.

- A short bridge from financials to the corporate tax return.

If a reviewer asks for a line from the return, you can pull the ledger, the sample invoice, the contract, and the bank proof without a hunt. That is audit-ready.

Your month-end close, upgraded for tax

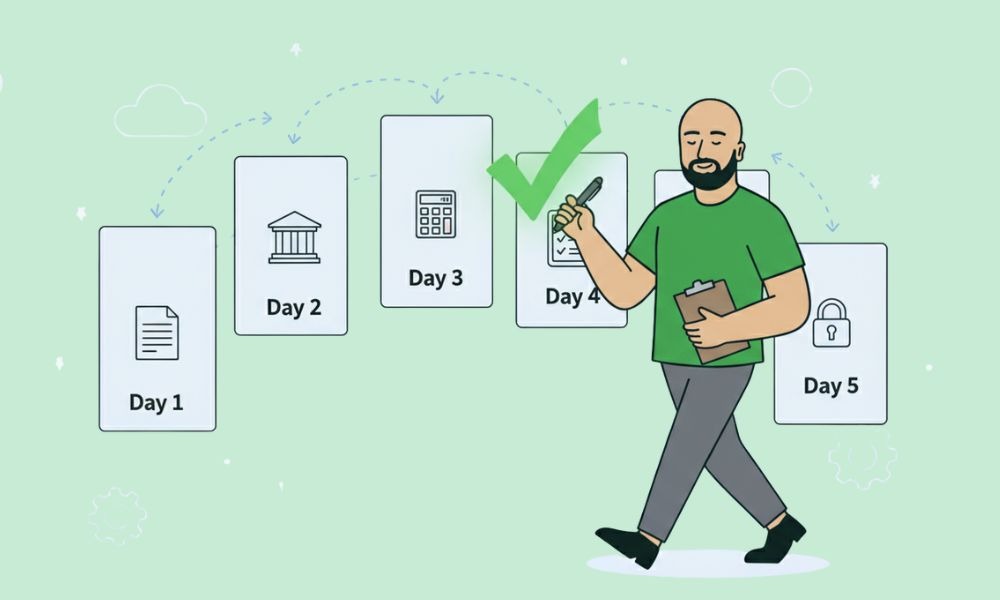

A five-day close that fits most teams

Day 1

Close sales and purchases. Code bank items. Chase missing documents.

Day 2

Reconcile bank and control accounts. Clear obvious suspense items.

Day 3

Review revenue cut-off, WIP or inventory roll-forwards, and fixed asset additions.

Day 4

Post final journals. Reconcile VAT control to the filed periods.

Day 5

Lock the period. Export the report pack. Save it to the period folder.

What goes in the period folder

- Trial balance and tie-out to management accounts.

- Bank reconciliations with statements.

- Revenue cut-off checks and sample proofs.

- AP and AR aging with actions.

- Fixed assets roll-forward and support.

- VAT control account tie-out to the return.

- If relevant, a mini transfer pricing note for related-party charges.

- A one-page “judgment notes” file.

Keep file names readable. Use one index file at the top of the folder that says where everything lives.

IFRS and your tax return: build the bridge

The clean bridge, step by step

- Start with the final trial balance for the period.

- Map each account to a return line.

- List tax adjustments, with a one-line reason and a link to support.

- Tie the rounded amounts in the return back to the exact trial balance numbers.

- Save the bridge as a PDF and keep the working file behind it.

Common adjustment buckets to label clearly

- Non-deductible expenses you have identified.

- Depreciation differences if your policy yields timing gaps.

- Related-party interest or service fees with support.

- Provisions or fair-value movements that need a specific tax treatment.

The goal is simple. Any reviewer can land on a return line and see the math and the proof in one minute.

Special notes for 2025 audit requirements

- Revenue over the threshold? Prepare and maintain audited financial statements from your first 2025 tax period.

- Qualifying Free Zone Person? Keep audited financial statements for the period, and follow any extra procedures that apply to your activity.

- Part of a tax group? Prepare audited special-purpose financial statements in the format the Authority sets.

- Non-resident with UAE nexus? When testing any revenue threshold, use only UAE permanent establishment or nexus revenue.

If your 2024 approach relied on earlier rules, refresh your 2025 plan. The scope is different now.

Controls that cut audit time in half

- Lock prior periods. No edits after filing without a one-line change note saved to the folder.

- Least privilege. Only the people who need access have it. Review user lists quarterly.

- New vendor guardrail. One person creates, a different person approves.

- Bank approval rails. Set approval levels by value. Keep a register of approvers and limits.

- Document retention. Seven years is a practical benchmark many UAE businesses follow. Save a cloud copy.

These are small moves. Together they tell a solid story to auditors and reviewers.

The 90-minute “audit rehearsal”

Pick a closed period. Pretend you just received a notice. In 90 minutes:

- Export the trial balance and the tie-out to the return.

- Pull five sales samples and five purchase samples with full proofs.

- Export bank reconciliations and statements.

- Open your judgment notes and related-party memo.

- Check your folder index. Fix any broken links.

You will see exactly where to sharpen your process before a real review lands.

Tools that keep the process light

You do not need a big stack. You need a clean workflow.

- Accounting platform with reliable bank feeds and a hard period lock.

- Shared drive with a consistent year-period structure and an index file.

- Simple OCR for bills and receipts so sources live with entries.

- Close checklist saved in the folder, ticked and dated each month.

- Sampling tracker that remembers which items were tested and what was missing.

Choose tools your team already knows. Speed beats features. Many Corporate tax filing services providers also recommend lightweight, disciplined tool stacks that work equally well for Free Zone operations and Corporate Tax Free zone compliance.

Common pitfalls we see, and quick fixes

- Old suspense items hanging around. Clear them monthly and write a one-line note for anything that rolls.

- Manual journals at the last minute. Post earlier, keep narrations precise, and attach support.

- No owner for the audit pack. Name a coordinator. Give them a shared inbox for notices and requests.

- Loose related-party pricing. Keep one page that explains the rate and the logic, plus a couple of comparables if you have them.

- Mixing Free Zone and mainland flows. Tag each invoice and keep the evidence where it can be found in seconds.

Reporting calendar you can copy

Month-end

Day 1–2: code, reconcile, chase documents

Day 3: review cut-off, WIP, and control accounts

Day 4: post finals, tie VAT control to returns

Day 5: lock, export, file the pack

Quarter-end extras

Ten-item sampling test, related-party memo refresh, AR and AP clean-up

Year-end

Update judgment notes, bridge to the corporate tax return, archive with an index

Two quick ways we can help

Talk to Alpha Pro Partners for a 2025 audit-readiness check. We map your obligations, review your close, and hand you a one-page plan.

Need a file that explains itself? We build the folder structure, the close checklist, and the return bridge, then coach your team through the first cycle.

FAQs

Do we need audited financial statements in 2025?

If your revenue crosses the threshold, yes. Also yes if you are a Qualifying Free Zone Person. Tax groups prepare audited special-purpose financials. If you are not sure where you sit, we can check your facts and confirm your status.

When do the new audit requirements kick in?

From tax periods that start on or after 1 January 2025.

What if we are a tax group?

Prepare audited special-purpose statements in the form the Authority sets, then build your return bridge off that base.

How should we handle related-party charges?

Keep signed agreements and a short support note showing how you set the rate. Tie charges to services delivered.

How do we prove revenue cut-off at year end?

Keep signed completion notes or delivery proofs, match them to invoices and cash, and lock your schedule in the period folder.

What if we adjust a filed period?

Document the reason, the fix, and the date. Keep the note with your return support pack.

How long should we keep records?

Keep enough to cover reviews and audits for the full retention window. Seven years is a practical benchmark many UAE businesses follow.

Can we rely on management accounts for the return?

Your return should tie back to your audited, or final, financial statements for the period. Use a clean bridge that shows every step.

We are a Free Zone entity. Anything extra?

If you claim a special regime, keep evidence that your activities meet the conditions, and follow any additional procedures that apply to your activity.

What is the fastest way to get audit-ready now?

Name a coordinator, run the 90-minute rehearsal on a closed period, clean reconciliations, and build a simple bridge from financials to the return.

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.png)

.png)

.png)