What Small Businesses Need to Know About the Latest UAE VAT Regulation Changes (2025 Update)

Why this update matters in 2025

We know VAT can feel heavy when you are trying to run a lean team. The good news is the core rules in your source material are stable and clear. The standard rate remains five percent. The Federal Tax Authority continues to manage registration, filings, collections, and refunds. Your job is to apply the rules to your supplies, keep clean records, and file on time.

This update brings the essentials together in one place. Everything here comes from the sources you shared. There is no extra interpretation. We have simply organised the points so a busy owner can understand the steps and act with confidence. Professional help from experts who provide corporate tax services in UAE or vat filing services can also make compliance easier for small teams.

VAT basics in plain words

VAT is an indirect tax on most supplies of goods and services. It sits in the price you charge and the price you pay. You collect VAT from customers and pay VAT to suppliers. At filing time you report both. The difference goes to the government or comes back as a refund if input VAT is higher.

Key points to hold in mind:

- VAT is charged at each stage in the supply chain.

- Consumers carry the cost. Businesses are the collectors and the record keepers.

- The standard rate in the UAE is five percent.

- Over one hundred and fifty countries use VAT or a similar system.

Who runs VAT in the UAE

The Federal Tax Authority manages VAT across the country. It handles registration, collects tax and fines, processes refunds, and provides guidance. It also works with the Ministry of Finance to support economic diversification and stable public revenue.

For small businesses this means you work within one framework. You register once. You file online. You keep records the FTA can review if needed. Many companies also rely on tax consultancy UAE experts who can guide them on both VAT and corporate tax services in UAE for smooth compliance.

Do you need to register in 2025

Your sources set two clear thresholds:

- Mandatory registration when your taxable supplies and imports are above AED 375,000 in a twelve month period.

- Voluntary registration when your supplies and imports are above AED 187,500. You may also register when your expenses exceed AED 187,500. This helps start-ups recover input VAT even when revenue is low.

If you think you are below the thresholds you should still maintain full financial records. The FTA can check if you should have registered. A good vat filing services provider ensures you never miss deadlines or thresholds.

What registration changes day to day

Once registered you:

- Charge VAT on taxable goods and services you supply.

- Reclaim input VAT on business costs that relate to your taxable or zero rated supplies.

- Keep accurate records that show how you calculated VAT.

- Report VAT you charged and VAT you paid on a regular schedule through an online submission.

- Pay the net amount when output VAT is higher or request a refund when input VAT is higher.

The rhythm is simple. Record. Review. File. Pay or claim.

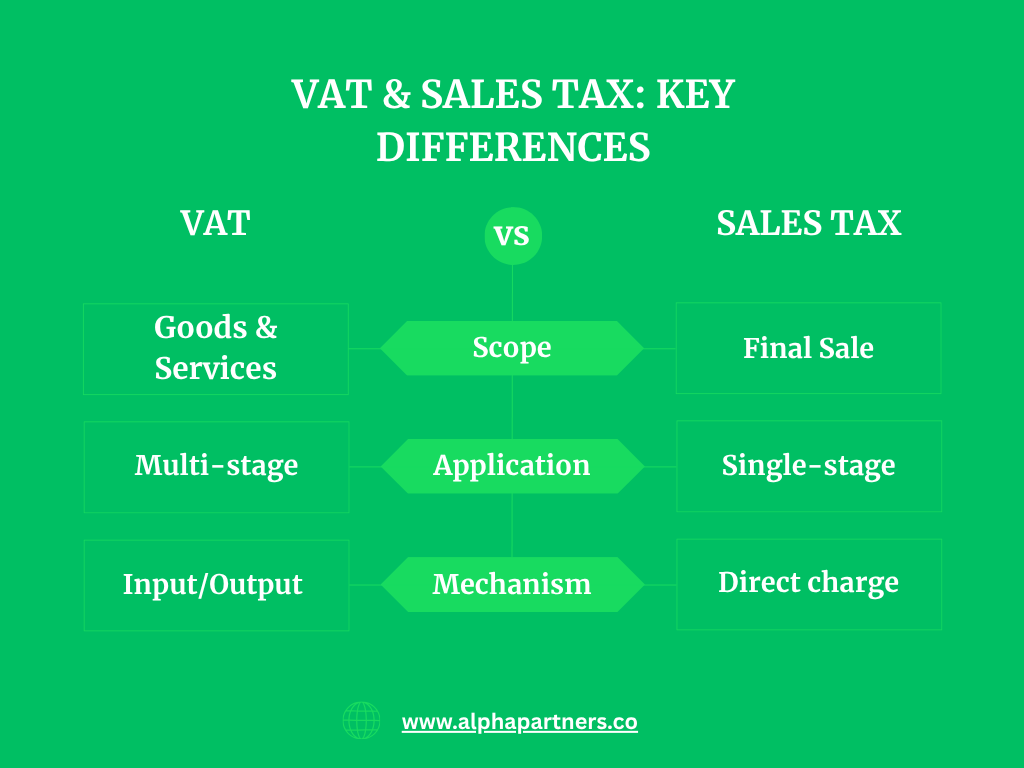

VAT versus sales tax

For your team and your customers the two can look similar. The difference sits in how each system works:

- Sales tax is often limited to the final sale and often to goods.

- VAT applies to goods and services across the supply chain, including imports.

VAT is built to match values created at each step. That is why it uses input VAT recovery and output VAT charged to arrive at the net due.

Zero rated supplies at a glance

Your sources list the main zero rated categories:

- Exports of goods and services to outside the GCC

- International transportation and related supplies

- Supplies of certain sea, air, and land means of transport

- Certain investment grade precious metals of high purity

- Newly constructed residential properties supplied for the first time within three years of construction

- Certain education services and related goods and services

- Certain healthcare services and related goods and services

Zero rated means you charge zero percent but you still recover input VAT that relates to these supplies.

Exempt supplies in simple terms

Exempt categories in your sources include:

- Some financial services as clarified in VAT legislation

- Residential properties

- Bare land

- Local passenger transport

Exempt means you do not charge VAT. It also means input VAT recovery is restricted when costs relate to exempt supplies.

Partial exemption without the jargon

Many small businesses have mixed activity. Some lines are taxable or zero rated. Some are exempt. When one cost supports both sides you need to apportion input VAT.

Your sources say you should use an input tax ratio as a starting point. A different method can be used if it is fair and agreed with the FTA. The important part is to document how you did the split and keep the backup.

Real estate treatment kept short

- Commercial property sales and leases are taxable at five percent.

- Residential property supplies are generally exempt.

- The first supply of a new residential property within three years of construction was zero rated at the time VAT was introduced.

Tie your treatment to the type of supply. That is the safe way to stay aligned with your sources.

Government entities and VAT

Supplies by government entities are generally within VAT so that private and public suppliers compete on the same terms. Some activities are outside the scope where there is no competition or where the entity is the sole provider. Certain entities can receive VAT refunds to avoid budget issues.

The tax treatment follows the supply itself. It does not change simply because the buyer is a government body.

Your 2025 VAT action plan

Use this sequence to keep things calm and simple.

1. Confirm your status

- Review the last twelve months of taxable supplies and imports.

- If above AED 375,000 prepare to register.

- If above AED 187,500 in supplies or expenses consider voluntary registration to recover input VAT.

2. Map your supplies

- List each product or service.

- Assign a treatment based on your sources: taxable, zero rated, or exempt.

- Note the evidence you will keep for each line such as contracts and invoices.

3. Set up invoicing and receipts

- Include VAT details on invoices for taxable and zero rated supplies.

- Keep supplier invoices that show VAT charged so you can reclaim input VAT correctly.

- Store documents in a simple structure so you can find them fast.

4. Track input VAT by purpose

- Tag each cost to the supply it supports.

- Separate costs that relate to exempt activity.

- Prepare a simple worksheet for any partial exemption split.

5. File on time

- Prepare returns online as required by the FTA.

- Recheck totals for output VAT and input VAT.

- Pay the net amount or request a refund if input VAT is higher.

6. Keep records ready

- Maintain financial records that match your return figures.

- Save invoices, receipts, and any apportionment working papers.

- Be ready to support your position if the FTA asks for proof.

Need help turning this plan into a clear checklist for your team

Contact Alpha Pro Partners for a simple VAT workflow that follows your sources and keeps filings smooth.

Common pain points and how to fix them

We have seen the same issues trip up small teams. The fixes are simple when you stick to your sources.

Mixing up zero rated and exempt

Zero rated still allows input VAT recovery. Exempt does not. If you are not sure where a supply sits, read the list again and match the definition to your supply. Keep a short note on file to show why you chose that treatment.

Missing documents for input VAT

If you plan to reclaim VAT on a cost, keep the invoice that shows VAT charged. If you cannot find the document, do not reclaim the VAT until you obtain a valid copy. This simple rule avoids later adjustments.

Poor tracking for mixed use costs

If a cost supports both taxable and exempt supplies, note the percentage used for each. Apply your input tax ratio to split the VAT. Save the working paper. When the method is fair and clear, reviews are easier.

Treating all real estate the same

Commercial and residential are not the same for VAT. Identify the supply type first. Then apply the correct rule.

Records that do not match returns

If your returns do not align with your records, you will spend time fixing gaps later. Align totals, invoice counts, and adjustments before you file.

A simple record keeping setup

You do not need a complex system to stay compliant. A small structure works well when everyone uses it the same way.

- One folder for sales invoices by month.

- One folder for purchasing invoices by month.

- A log for exports, international transport, and other zero rated items where you keep proof.

- A short file note for each exempt line to explain the treatment.

- A worksheet for partial exemption splits with the ratio you used.

When your team knows where things live, filings are faster and reviews are calmer.

A friendly reminder for 2025

Keep the basics tight. Know your threshold. Map your supplies. Track input VAT by purpose. File on time. Save your documents. Everything else flows from these steps.

Need help building a VAT map that your team can follow

Contact Alpha Pro Partners. We can structure your supply list into taxable, zero rated, and exempt, and set up a simple record trail that matches your sources.

FAQ

What is the VAT rate in the UAE

Five percent is the standard rate. That is the rate you use for most taxable supplies.

Who oversees VAT

The Federal Tax Authority manages VAT. It handles registration, returns, collections, refunds, and guidance.

When is VAT registration mandatory

When taxable supplies and imports exceed AED 375,000 in a twelve month period.

Can I register voluntarily

Yes. You can register when supplies and imports exceed AED 187,500. You can also register when expenses exceed AED 187,500. This option helps new businesses recover input VAT sooner.

What is zero rated versus exempt

Zero rated is a tax rate of zero percent where you still recover input VAT. Exempt is outside VAT for output and restricts input VAT recovery when costs relate to those supplies.

How do I handle costs that support both taxable and exempt supplies

Use an apportionment method. Your sources point to an input tax ratio as the first approach. Use another fair method only where agreed with the FTA. Keep the working papers.

Does VAT apply only to goods

No. VAT applies to goods and services. That is a core difference from many sales tax systems.

What should I keep for a refund claim

Keep the invoices that show input VAT. Keep proof for zero rated supplies. Make sure your records align with your return totals.

Do I need to keep records if I am under the threshold

Yes. Your sources say all businesses should keep accurate financial records. The FTA may need to check whether you should have registered.

How should I treat real estate

Commercial supplies are taxable at five percent. Residential supplies are generally exempt. The first supply of a new residential property within three years at the time of VAT introduction was zero rated.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpg)

.jpg)

.png)

.png)

.png)